How to invest

The importance of diversifying your investment portfolio

What is portfolio diversification?

Portfolio diversification is the most basic and effective way of reducing investment risk. A well-diversified portfolio contains a mix of asset types and investment vehicles used to limit exposure to any single asset or risk. The rationale behind this technique is that a portfolio constructed of a variety of assets will, on average, have a lower portfolio risk than any incumbent holding or security.

Diversification attempts to smooth out unsystematic risk events (non-market wide events) in a portfolio, ie. sizable gains will help offset losses in other areas. The benefits of diversifying your investment portfolio hold only if the underlying investments in a portfolio are not correlated—that is, they respond differently, often in opposing ways, to market influences.

Why & when should you diversify your investment portfolio?

As investors, we can't all be expert evaluators of investments, nor do we have the wherewithal to dedicate our time to the vocation of allocating capital. However, creating an optimal strategy to grow our wealth and work towards financial independence is something everyone strives for. This is why most investors should make diversification part of their long term investment strategy.

“The only investors who shouldn’t diversify are those who are right 100% of the time.” - Sir John Templeton

Risk Management

One of the most important and influential economic theories dealing with finance and investment by Harry Markowitz is taught to all business students in the early years of their degree. The school of thought advocates diversifying investments and highlights the benefits of not putting all your eggs in one basket. Investments face both systematic risk—market risks such as interest rates and recessions—as well as unsystematic risk—issues that are specific to each investment, such as management changes or poor product sales.

The key takeout from this theory is that proper portoflio diversification can't prevent systematic risk, but it can dampen, if not eliminate, the unsystematic risk from an investor's portfolio.

Preserving capital

The preservation of capital should be the basic starting point for all investors. Not all investors are in the capital accumulation phase of life; some close to retirement have goals oriented towards the preservation of capital, and portfolio diversification can help protect your savings. Diversification does this by limiting investors exposure to an individual investment loss.

Avoid losses at all costs. While this may sound like a common-sense approach, many investors develop strategies failing to adequately protect themselves against permanent capital loss. Diversifying investments becomes a foundation pillar for an investor looking at protecting their portfolio from losses.

Generating stable returns

At the core of a well-diversified portfolio is choosing investments that react differently to the same economic environments. Although an investor won’t achieve the abnormally high returns from owning just one high-flying stock, they will also not suffer its ups-and-downs either. In effect, an investor will earn the weighted average return on their underlying investments but is not fully exposed to the volatility (risk) of any particular investment. This is particularly important for those with a short investment horizon.

Methods of diversifying your investment portfolio

Diversification comes from investing in products that are inherently different from each other in terms of their risk profiles. Within the investment landscape, the most common ways to spread risk (diversification) is to invest in products that vary across asset class, sector, industry, region, size, and income profile. Given Jasper’s expertise in bringing real estate and, in time, other alternative assets to the market, it is worth illustrating how real estate can be used as part of a wider diversified investment strategy.

1. Asset class diversification

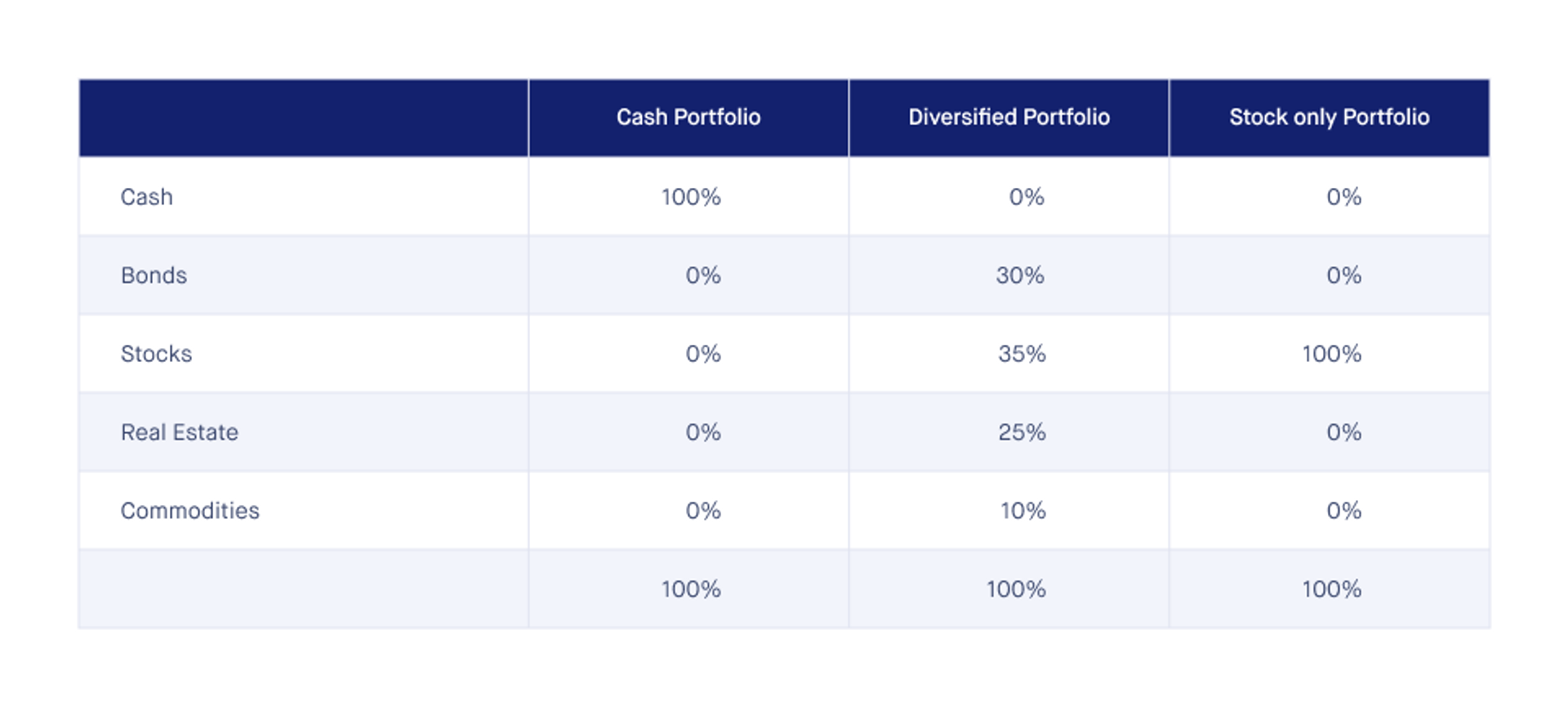

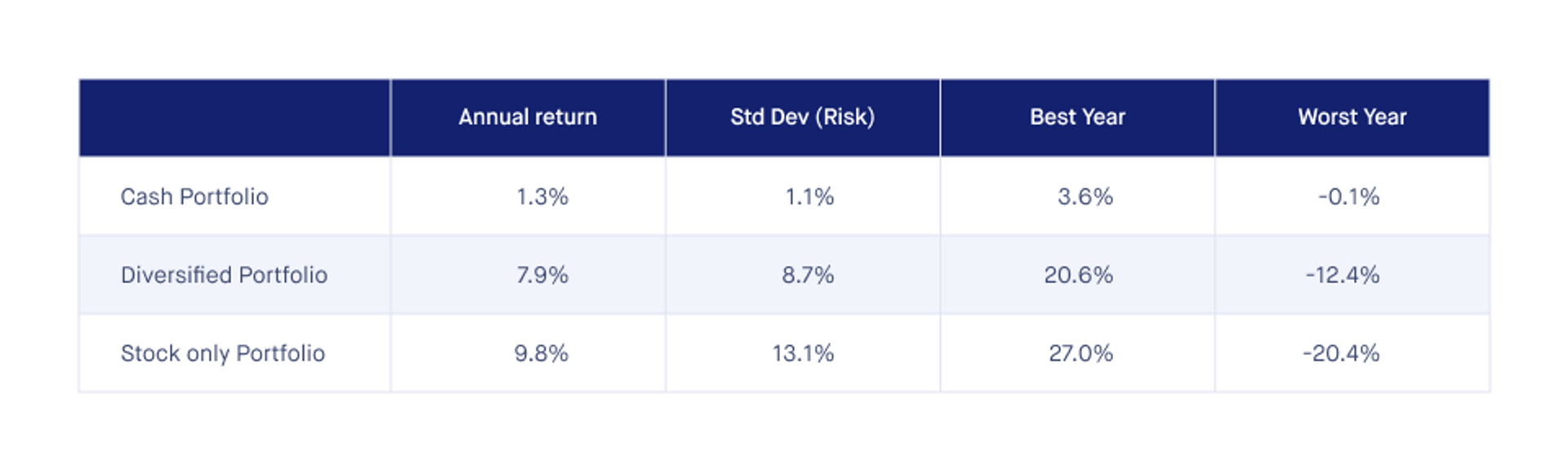

In the same way, nutritionists recommend a balanced diet;investment advisors recommend a balanced portfolio. The more food groups on a person's plate, the more nutrients a person’s body consumes and the healthier that person is. Likewise, an investor looking to create a healthy portfolio should choose assets across various classes. Traditional asset classes available to investors are stocks, bonds, exchange-traded funds (ETFs), commodities and to a lesser extent real estate. Each is exposed to unique asset-level risks and are not all perfectly correlated to each other. Fig. 1 illustrates how a diversified portfolio can achieve better performance (in some cases) and a lower risk profile than investing in a single asset class. The analysis was carried out over the last decade and consisted of purely hypothetical portfolios that utilised actual market data to model returns.

The hypothetical portfolio analysis illustrates the outcome of a robust diversification strategy, protecting an investor against fluctuations in the market. Considering the hypothetical portfolios constructed, as expected, storing cash under your bed returned the least since 2010 but was the most stable while putting all an investor’s eggs into one basket (global equities) proved to be the most volatile. The diversified portfolio returned slightly less than the stock-only portfolio but was less exposed to market fluctuations over the last decade.

2. Sector diversification

In particular cases, an investor may understand and be comfortable with only one asset class or wish to have a more diversified portfolio within a particular asset class. Given that investor’s knowledge, they may choose to remain within their circle of competence and achieve diversification in investing within that asset class. Here is where sector diversification comes into play. Let's take an investor who has chosen to allocate capital towards real estate and is looking to evenly spread their portfolio risk within this asset class. This investor may then choose to invest in 25% residential, 25% office, 25% retail and 25% industrial sectors.

A study by Dong and Li, 2012, compared different cross-sector diversification strategies in different economic phases in New Zealand. The study found the best diversification strategy may not be consistent over different economic phases and that industrial property in Auckland performed the best across the study period (2002-2010). Conventional wisdom says that property sectors do not respond synchronously to economic shocks. For an investor who is diversified by sector, this means they have limited their exposure to single economic shocks and improve their flexibility to rebalance their portfolio and better respond to economic events.

3. Industry/Size diversification

At a base level, any investment represents a determination that the underlying economics of an asset will do well. Different assets perform differently in the same economic conditions. Diversification by industry and size is useful for an investor looking to limit their exposure to a certain industry. Broad industry sectors include cyclical (financial services and real estate), defensive (healthcare and utilities) and sensitive sectors (energy and industrials). This form of diversification adds an additional layer of risk reduction to an investor’s portfolio.

4. Geographical diversification

Geo-political and geographical risks are becoming increasingly important considerations for investors when analysing the riskiness of their portfolio. Blackrock, the largest global asset manager, is undergoing a significant revamp of its investment strategy to make sustainability the “new standard for investing”. This highlights both the increasing need for socially responsible investing and also the recognition that climate change poses a real risk to long-term economic viability of investment portfolios. For investors, having investments in various parts of the world reduces risks of unpredictable natural disasters or an adverse change in the political environment severely impacting their portfolio.

5. Income profile diversification

A lesser-known method of portfolio diversification is by income profile. This relates directly to the underlying nature of cash flows derived from an investment. The method is particularly important when considering an investor’s wealth goals. People are accustomed to thinking about their savings in terms of goals: retirement, college, a down payment on their first home. An assessment of investment horizon and risk appetite will guide an investor toward the right investment product. Investments are a function of income production and future capital gains. Capital gains are inherently riskier given higher uncertainty and are often only realised further into the future compared to income streams from an investment.

All investments will fall on an income-capital gains continuum. An investor should pick a balance of income-producing and growth assets in their portfolio suited to their underlying wealth objectives. It is typical to observe that as an investor matures, their investment horizon shortens, and the requirement of income-producing assets increases as they approach retirement. For example, an investor who typically invests in risker residential apartment developments may choose instead to invest in stable yielding, passive industrial properties that can supplement their retirement income.

Investment diversification as an ongoing process

Investors should carry out regular maintenance on their investment portfolio. This means:

1. Monitor

Evaluate your investments periodically for changes in personal circumstances, relative portfolio performance, and risk.

2. Rebalance

Revisit your investment diversification mix to maintain the risk level you are comfortable with and correct drift that may happen as a result of market performance. There are many different ways to rebalance; for example, you may want to consider rebalancing if any part of your asset mix moves away from your target by more than 10 percentage points.

3. Refresh

As an investor matures, their financial goals change, and so does their risk appetite. A prudent approach would require an investor to adapt their portfolio accordingly. At least once a year, or whenever your financial circumstances or goals change, revisit your plan to make sure it still makes sense.

For example, once you've entered retirement, a large portion of your portfolio should be in more stable, lower-risk investments that generate income. But even in retirement, diversification is key to risk management. At this point in your life, your biggest risk is outliving your assets. So just as you should never be 100% invested in stocks, it's probably a good idea to never be 100% allocated in short-term cash investments if your time horizon is greater than one year.

Key takeaways

Achieving your long-term goals requires balancing risk and reward. Choosing the right mix of investments and then periodically rebalancing and monitoring your choices can make a big difference in your outcome.

For investors looking to add commercial real estate to their portfolio, minimum equity requirements have made the class inaccessible or extremely hard to achieve portfolio diversification within the sector. However, when investing with Jasper, investors can put small amounts of money into several different commercial real estate investments and diversify their portfolio by sector, industry, size, geography and income profile. By design, the investor will have the unprecedented ability to achieve a level of diversification driven by their individual investment risk appetite. The ability to build a low-cost tailored portfolio allows investors to handpick various risk exposures based on their investment goals.

Ready to become an investor with Jasper? Click here to get started.

Vernon Sequeira

Investment Manager

Posted on 25 Feb 2020

Invest with us

Our expertise in acquiring and managing real estate assets, combined with our proprietary technology, helps us generate strong risk-adjusted returns for a diverse range of investors.

A strategic partner for institutional capital

Jasper is an experienced operating partner for family office and institutional investors wanting access to high-conviction real estate strategies across Australia and New Zealand. We co-invest alongside our partners in each joint venture.

We are proud of our track record and relationships with some of the biggest names in real estate, including Blackstone.

We make commercial real estate investment accessible to private investors in a simple and transparent way.

We provide private investors with curated opportunities, low minimums, transparent reporting and improved liquidity. All available through our secure online portal.

We manage the entire investment process for you from start to finish; you sit back and enjoy direct commercial property ownership and the passive income it can provide.

Read Important Disclosures

Important Disclosures

Liquidity Not Guaranteed: Jasper offers secondary market functionality on its platform from time to time, however, there is no guarantee that you will be able to exit your investments on the secondary market or at what price an exit (if any) will be achieved.

Performance Not Guaranteed: Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product made reference to directly or indirectly in this website will be profitable, or equal any corresponding indicated historical performance level(s).

Risk of Loss: Investing in commercial real estate involves a high degree of risk and may result in partial or total loss of your investment. We encourage our investors to invest carefully. We also encourage investors to get personal advice from your professional investment advisor and to make independent investigations before acting on information that we publish.

No Personal Advice: Jasper does not provide personal advice or recommendations. The information provided on this website is general in nature only and does not constitute personal financial advice. The information has been prepared without taking into account your personal objectives, financial situation or needs. It is important for you to consider these matters and to seek appropriate legal, tax, and other professional advice before making a decision.

Wholesale Offers: Jasper currently only offers financial products to wholesale (or other qualifying) investors. Jasper does not currently hold a Managed Investment Scheme (MIS) license and our products are not suitable for retail investors.

FSPR No. 692011. Information on this page is based on information available to us as of the date of posting and we do not represent that it is accurate, complete or up to date.